Zhejiang Robot Industry Association

Zhejiang University Robotics Institute

Golden Conference & Exhibition Group

Shanghai Top Sequoia Exhibition Co., Ltd.

Shanghai Berrick Exhibition Co., Ltd.

The year 2026 has been widely recognized as the official large-scale commercial mass-production year for China’s humanoid robot industry. Driven by national policy support, full-spectrum supply chain advantages and continuous technological iteration, the domestic humanoid robot sector has completely stepped out of the stage of prototype demonstration and small-scale trial operation, officially entering a new cycle of industrial-scale deployment and global market expansion. Equipped with the world’s most sophisticated high-end precision manufacturing cluster, Chinese humanoid robot manufacturers continue to lead the global market in terms of market share, mass delivery capacity and commercial implementation speed, forming the core growth engine of the global embodied intelligence robotics industry. Based on authoritative industrial data and research reports from MIIT, CCID Research Institute, Morgan Stanley and other institutions, China’s humanoid robot industry is maintaining exponential growth, providing strong support for global intelligent manufacturing upgrading, automated replacement of high-risk labor scenarios and the expansion of emerging overseas markets.

In 2025, China laid a solid and leading foundation for the global humanoid robot industry. Domestic manufacturers shipped 14,400 humanoid robots throughout the year, capturing 84.7% of the global market share, meaning more than 80% of humanoid robots worldwide are manufactured in China. The full industrial chain market size exceeded RMB 8.5 billion, covering complete machine manufacturing, core component R&D, embodied AI algorithms and customized industrial solutions. China has gathered more than 140 humanoid robot enterprises, among which Unitree Robotics and Agibots dominate the market, jointly accounting for over 75% of domestic shipments. At this stage, the industry was still in the pilot commercialization phase, with applications mainly concentrated in university scientific research and technical exhibitions, while large-scale industrial deployment remained limited, laying sufficient technical and production capacity reserves for the industrial explosion in 2026.

In 2026, the first year of formal mass production, the industry achieved leapfrog development with comprehensive breakthroughs in production capacity, market scale and commercial landing speed. According to official data from MIIT, China’s annual humanoid robot output will exceed 100,000 units in 2026, with a year-on-year growth of 594%, and the annual terminal delivery volume is expected to reach 50,000 units, occupying more than 90% of global deliveries. Benefiting from a core component localization rate of over 90%, the BOM cost of domestic humanoid robots has dropped significantly from RMB 500,000 in the early stage to RMB 140,000–200,000, and the affordable terminal price has greatly lowered the procurement threshold for various industries, breaking the long-term high-price monopoly of overseas high-end humanoid robots. With the full operation of 10,000-unit-level intelligent factories of leading enterprises, the industry realizes stable monthly delivery of 1,000 units. The number of standardized domestic application scenarios continues to expand, and more than 100 benchmark production lines for industrial, service and special scenarios are expected to be completed within the year, completing the essential transformation of humanoid robots from exhibition prototypes to practical industrial equipment. In 2026, the full-chain market size will exceed RMB 20 billion with an industry growth rate of 120%. From 2025 to 2030, the compound annual growth rate remains at 106%, far outperforming traditional industrial robots and new energy vehicle sectors.

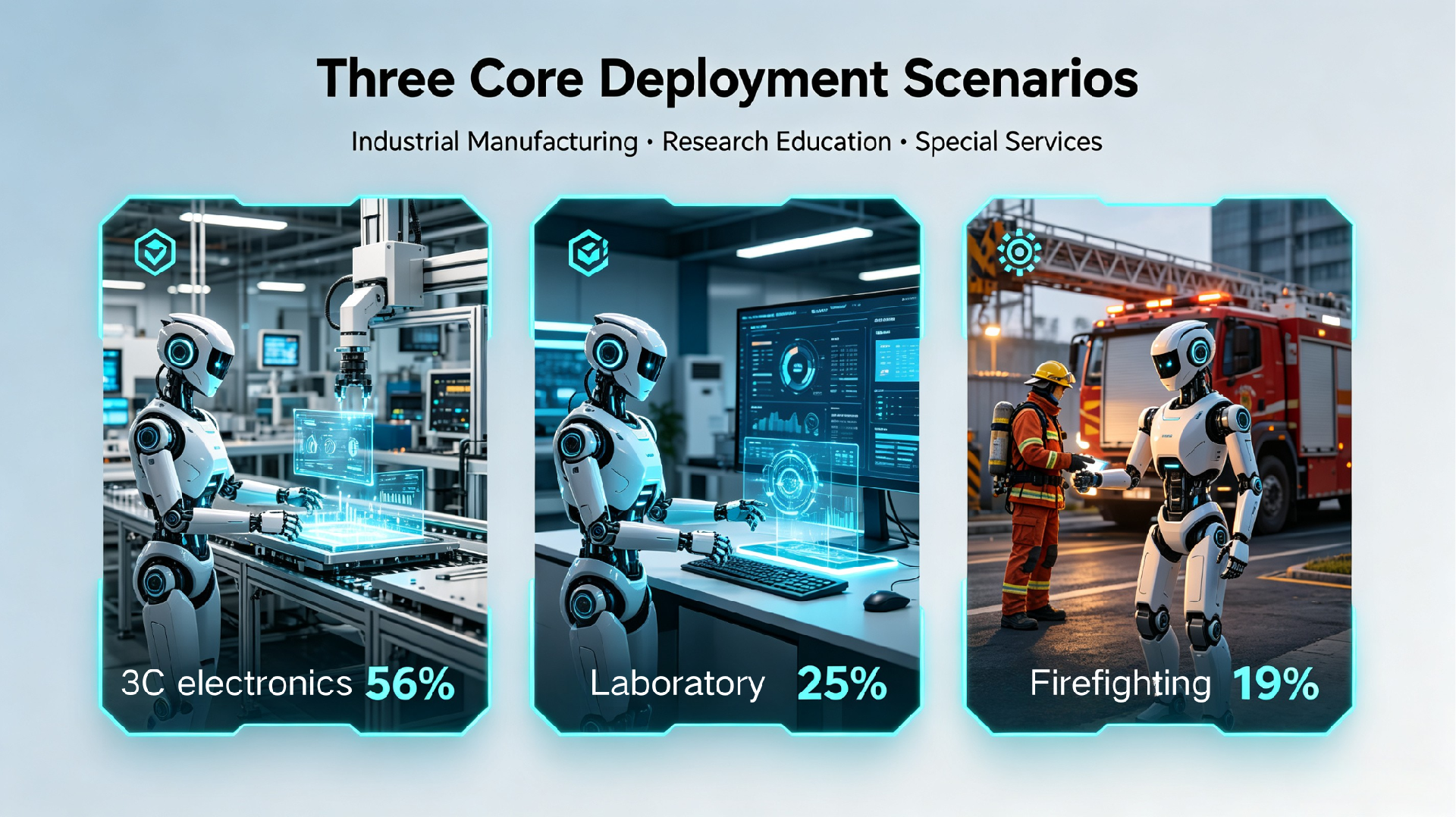

At present, the mass deployment of China’s humanoid robots has formed a stable multi-scenario operation system with increasingly clear commercialization paths. In industrial manufacturing, as of July 2026, more than 120 listed manufacturing enterprises have deployed humanoid robots in production lines for 3C electronics, new energy vehicle parts, warehouse logistics and other mainstream fields, replacing repetitive, high-intensity and high-risk loading, unloading, handling and quality inspection work. Industrial procurement orders account for 56% of annual shipments, serving as the core pillar of industrial growth. In scientific research and education, top domestic universities and AI laboratories continuously purchase domestic humanoid robots for embodied AI algorithm training and technical research. Meanwhile, overseas procurement demands from Europe, America and Southeast Asia have surged by 210% year-on-year. The scientific research track has become a stable cash flow source for the industry with high stability and profit margins. In special service scenarios, domestic humanoid robots have been widely applied in power inspection, fire emergency rescue, airport services and elderly care, with multiple models included in the municipal standardized procurement system, effectively filling the labor gap in high-risk and shortage service scenarios.

From 2026 to 2030, China’s humanoid robot industry will maintain sustained high growth, steady cost reduction and full-scenario popularization with continuous market expansion. Annual shipments will grow steadily, reaching 112,000 units in 2027, 207,000 units in 2028 and 446,000 units in 2030. China will maintain over 88% of global market share, with cumulative deliveries exceeding 1.14 million units from 2025 to 2030. The full industrial chain market size will grow synchronously, reaching RMB 425 billion in 2027, over RMB 718 billion in 2028 and RMB 1.48 trillion in 2030. A mature industrial structure has taken shape, with complete machine hardware accounting for 55%, core components 30%, and intelligent software and solutions 15%. In the long term, the full-chain market scale is expected to exceed RMB 1 trillion by 2035, making humanoid robots standardized flexible automation equipment for modern manufacturing and empowering the development of new productive forces.

Multiple driving forces support the long-term prosperity of China’s humanoid robot industry. China owns the world’s only complete upstream and downstream industrial cluster for humanoid robots, shortening component delivery cycles by 60% compared with overseas markets. Large-scale mass production continuously reduces manufacturing costs and builds irreplaceable industrial barriers. In addition, national “Robot Plus” action plans, special industrial funds and local procurement subsidies continuously stimulate domestic market demand and accelerate commercialization. The explosive growth of overseas demands further expands industrial increment. Labor shortages in European and American manufacturing, elderly care demands in aging Japan and South Korea, and automation upgrading needs in Southeast Asia’s transferred manufacturing industries drive a 210% year-on-year export growth of Chinese humanoid robots in 2026. Furthermore, continuous iterations of lightweight joint technology, vision-language-action models and low-latency teleoperation technology effectively solve traditional industry pain points such as insufficient precision and dexterity, greatly improving product practicability and scenario adaptability.

While the industry embraces broad long-term prospects, it still faces staged constraints. Technically, ultra-precise force control, long-distance low-latency teleoperation and medical-grade equipment transformation require further optimization. In terms of global layout, international certifications including EU CE, U.S. FDA and Japan MHLW involve long approval cycles, restricting large-scale overseas promotion. In terms of business operation, midstream complete machine manufacturers rely on capacity expansion to dilute costs and achieve profitability, making full industrial profitability difficult in the short term, while upstream component enterprises show more stable profit performance. Nevertheless, short-term industry challenges will not reverse the long-term upward trend. With the continuous improvement of technology, global compliance systems and commercial models, China’s humanoid robot industry will continue to lead the global market and become a core benchmark for China’s high-end manufacturing exports.